It takes 23 days from the submission of the application materials to the issuance of the trial by the CSRC. The IPO of Beijing-Shanghai High-speed Railway Co., Ltd. (hereinafter referred to as "Beijing-Shanghai High-speed Railway") has been experienced in the A-share market with an average initial review period of 9 months and nearly 400 companies waiting in line for listing, which truly shows a "high-speed railway speed".

The prospectus published by the Beijing-Shanghai high-speed railway on October 25, 2019 is 578 pages long, but it has not achieved many disenchantment functions. On the contrary, several "myths" have been added — — For example, there are only 67 employees who are retired, rehired and seconded, and the per capita assets under management are 2.792 billion yuan; More than 50 million train tickets are sold every year, with an average gross profit of 124 yuan per ticket; The company has a long-term loan of more than 20 billion yuan, and the annual interest expense is more than 1 billion yuan, but it is all credit loans without any collateral … …

Up to now, the Beijing-Shanghai high-speed railway has been operating safely for more than 8 years, sending 1.1 billion passengers. From the perspective of income, profit and large-scale operation level, Beijing-Shanghai high-speed railway is a well-deserved "golden route". Railways and trains seem to be ordinary means of transportation, but considering their important position in the national economy, many countries in the world have regarded them as the key carriers of economic and political games. In the second half of the 20th century, in order to introduce competition and stimulate development, the railway systems of the United States, Japan, Britain, France, Germany and other countries have experienced long and arduous commercial reforms. In the process of losing its state-owned color, the railway has also produced many innovative operating ideas and commercial products such as "separation of network and transportation" and "Shinkansen".

It is not easy to open China railway system with market mechanism. As we all know, in the past, the management and operation of the railway system in China has long concentrated the power of administrative examination and approval, road network and transportation management in the Ministry of Railways. Until around 2000, China started the railway reform, and the Ministry of Railways was divided into the State Railway Administration, which is mainly under administrative supervision, the China State Railway Group Co.,Ltd., which is mainly under the management of several local railway bureaus, and various franchised companies.

According to the prospectus, through this IPO, the Beijing-Shanghai high-speed railway hopes to raise up to 50 billion yuan. If the target is achieved, the Beijing-Shanghai high-speed rail will become the sixth largest IPO project in the history of A shares. It is also a phased product of the combination of national will and technological innovation after a long process of exploration, and it bears a crucial mission of China’s railway market-oriented reform: it must be broken in the link of "commercialization verification".

Beijing-Shanghai high-speed rail is the most profitable high-speed rail line in China.

Double definitions of "golden route"

The idea of Beijing-Shanghai high-speed railway can be traced back to a series of internal discussions in the 1980 s. In 1990, the former Ministry of Railways assembled all the early studies into the "Concept Report of Beijing-Shanghai High-speed Railway Line Scheme", and formally put forward the idea that "China should also build high-speed railway". It was not until April 18, 2008 that the entire Beijing-Shanghai high-speed railway was officially started, and it was completed and opened to traffic on June 30, 2011.

In the project proposal approved by the State Council in 2006, it was mentioned that the total budget of Beijing-Shanghai high-speed railway would exceed 160 billion yuan. However, in the feasibility study report released one year later, the construction budget rose to 220.94 billion yuan, equivalent to a cost of 167 million yuan per kilometer. This also makes the Beijing-Shanghai high-speed railway the infrastructure project with investment scale second only to the Three Gorges Dam since the founding of New China.

80% of the lines have to be carried by new viaducts, and the demolition costs involved along the way are the main reasons for the high construction cost of Beijing-Shanghai high-speed railway. The cost of land acquisition and demolition in seven provinces and municipalities directly under the central government across the Beijing-Shanghai high-speed railway was not confirmed by audit until 2015. According to the contents of the prospectus of Beijing-Shanghai high-speed railway, the total cost of land acquisition and demolition reached 37.099 billion yuan. In addition, according to the prospectus, the construction capital of high-speed railway station reached 1.94 billion yuan.

These upfront investments were later directly realized in the form of capital into the shares of provinces and cities along the way in the Beijing-Shanghai high-speed railway company. At present, in addition to the above-mentioned local shareholders, the other three major shareholders of Beijing-Shanghai High-speed Railway are China Railway Investment Co., Ltd. (which invested 60.3 billion yuan when it was launched, holding 49.76%), Ping An Asset Management Co., Ltd. (which invested 16 billion yuan when it was launched, holding 11.44%) and National Social Security Fund (which invested 10 billion yuan when it was launched, holding 7.15%).

At the initial stage of operation, the Beijing-Shanghai high-speed railway is often compared with the "Beijing-Shanghai Express" route invested heavily by Air China, China Eastern Airlines and other airlines, because both of them connect the transportation services of the two most important cities in China. In fact, the difference between them is very obvious — — The Beijing-Shanghai express line is only to realize the rapid direct connection between business travelers in Beijing and Shanghai, and the Beijing-Shanghai high-speed rail is of great significance to the population flow and regional economy in the areas covered by the site.

A working paper (summary paper) published by the World Bank in 2014 also confirms this view — — The Beijing-Shanghai high-speed railway is 1318 kilometers long, but the proportion of passengers who take the whole Beijing-Shanghai high-speed railway line from beginning to end is not as high as expected, and the average ride distance is actually about 500 kilometers. If you start from Shanghai, this number can reach Bengbu City in Anhui Province. Starting from Beijing, you can reach Tai ‘an City in Shandong Province.

The total population living in provinces and cities along the Beijing-Shanghai high-speed railway accounts for 27.3% of the national total. The labor force can flow quickly and conveniently, which is conducive to promoting the economic development of provinces and cities along the high-speed rail. In another research report, the World Bank calculated the GDP of Dezhou and Jinan in Shandong Province in 2010, and concluded that the Beijing-Shanghai high-speed railway boosted the GDP of these two cities by 0.67% to 1.39% and 0.36% to 0.75% respectively in 2015.

This may be one of the most intuitive explanation cases of "when a train rings, there are two thousand gold".

China version of "separation of network and transportation"

A high-speed railway itself is a valuable fixed asset, plus station buildings, electrical equipment, land use rights and a small amount of cash along the line that can be estimated — — These constitute most of the assets of the listed Beijing-Shanghai high-speed rail company. The train assets running on this railway belong to the three local railway bureau groups of Shanghai, Jinan and Beijing along the Beijing-Shanghai high-speed railway.

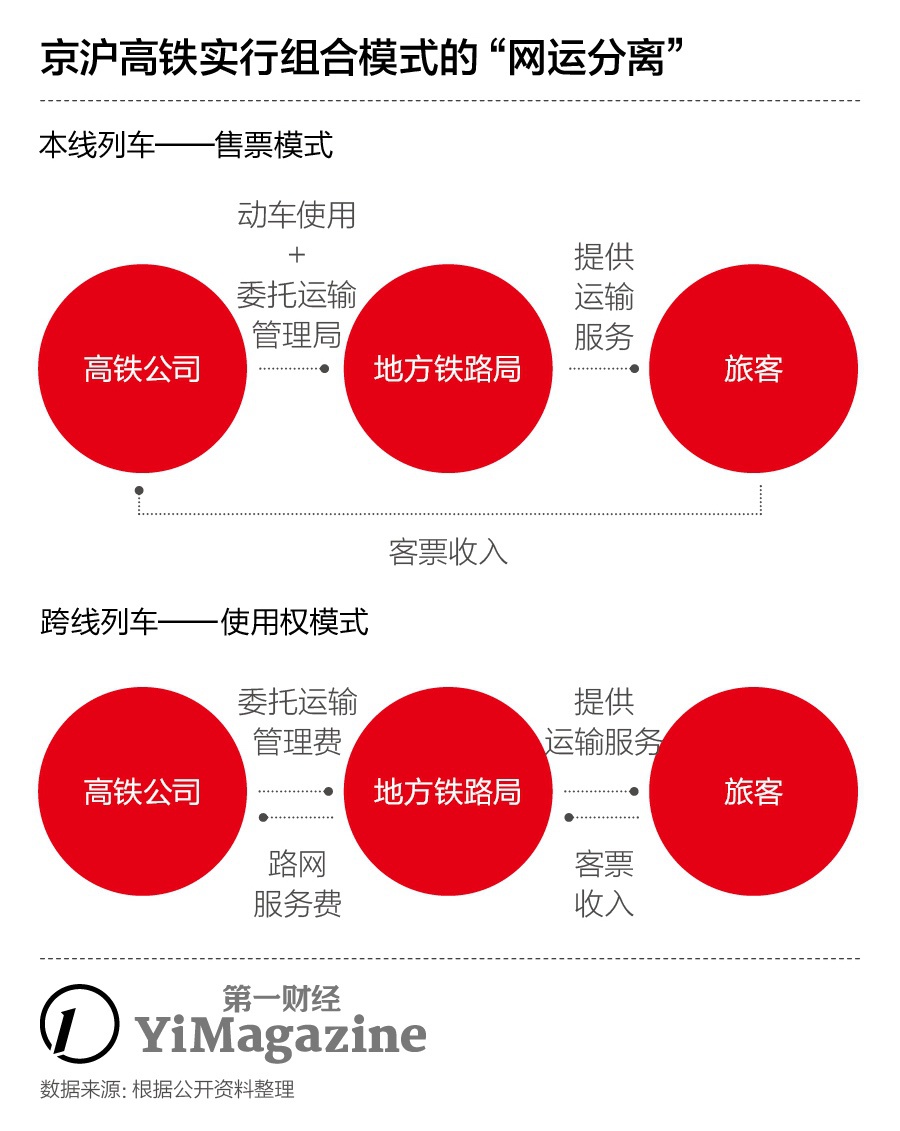

Based on the above division of assets, the relationship between Beijing-Shanghai High-speed Railway Company and railway bureaus along the line is generally a so-called "entrusted transportation" cooperation relationship, that is, the road network company entrusts railway bureaus with trains and workers to complete transportation services. In the transportation industry, this model is called "separation of network and transportation".

The idea of "separation of network and transportation" is to separate the railway network infrastructure with resource monopoly from the railway passenger and freight transportation with market competitiveness by setting up their own companies to operate. Its value lies in promoting the maximum utilization of road network resources with the help of increasingly flexible market-oriented passenger and cargo transportation business.

Germany is one of the representative countries that implement railway "separation of network and transportation". In addition to the state-owned Deutsche Bahn, there are currently more than 400 private railway operators who can use the German railway network, achieving full competition in the freight and short-distance passenger transport markets.

Theoretically, Beijing-Shanghai high-speed railway, as a road network company, has the right to collect the road network service fee from the railway bureau to which the trains operating on the road network belong — — Simple understanding is "toll", but the ticket revenue and the revenue generated by various services on the train belong to several local railway bureaus. In the prospectus, the Beijing-Shanghai high-speed railway directly refers to the local railway bureau as its "customer".

This situation is similar to that of long-distance buses running on expressways — — Whether it is empty or full, the highway company will charge the same toll; However, the passenger’s ticket money is handed over to the bus operating company, so what the passenger transport company needs to consider is to improve the attendance rate by improving the service experience, thus driving the continuous growth of ticket revenue.

The Beijing-Shanghai high-speed railway finally implemented a more complicated mode of "separation of network and transportation". As a result, the company not only collected tolls from the local railway bureau, but also had a part of the direct income of train tickets.

According to the prospectus, the Beijing-Shanghai High-speed Railway Company has signed the Agreement on Train Undertaking of Beijing-Shanghai High-speed Railway with Shanghai Railway Bureau, Jinan Railway Bureau and Beijing Railway Bureau, and the Beijing-Shanghai High-speed Railway has the service management right of "local trains", so it can obtain the ticket income of these trains.

The definition of "local train" by Beijing-Shanghai High-speed Railway is "a train running on the Beijing-Shanghai High-speed Railway, which starts and ends". Simply explained, the starting station and the terminal station of the train are all stations in a city along the Beijing-Shanghai High-speed Railway, such as Beijing to Nanjing, Jinan to Xuzhou and Tianjin to Shanghai.

For the trains on this line, the local railway bureau is the "entrusted service provider" of Beijing-Shanghai high-speed railway company, and its main income items are the train rental fee and entrusted service management fee paid by the latter (all train service personnel belong to the local railway bureau); At the same time, the local railway bureau does not have to pay "tolls" to the railway bureau.

The opposite of "local train" is "cross-line train", which refers to those trains whose starting station or terminal station is not on the Beijing-Shanghai high-speed railway, but will pass through (use) a certain section of the Beijing-Shanghai high-speed railway. For example, the high-speed trains from Zhengzhou to Nanjing or Beijing to Hangzhou are all over-the-line trains. For cross-line trains, Beijing-Shanghai High-speed Railway Company only participates in the operation as a simple road network operator, and collects "toll" from the local railway bureau to which the train belongs, and all the fare income belongs to the latter.

The combined "separation of network and transportation" that "the road network company collects both tickets and tolls" around the operation of Beijing-Shanghai high-speed railway is full of China characteristics. In other words, this is a phased achievement in the long journey of railway reform in China.

In fact, along with it, the discussion on the advantages and disadvantages of "separation of network transportation" in the industry has never stopped. On the one hand, this model is recognized, because it faces the intertwined railway operation system from the system. First, it makes a complete cut of "road network resources" and "transportation services". However, it is difficult to see the possibility of introducing other market-oriented railway operation service providers in the short term, so after the above-mentioned cutting, the process reengineering is still implemented among various state-owned companies, which increases the transaction cost and is a negative impact on improving system efficiency.

Balanced performance space

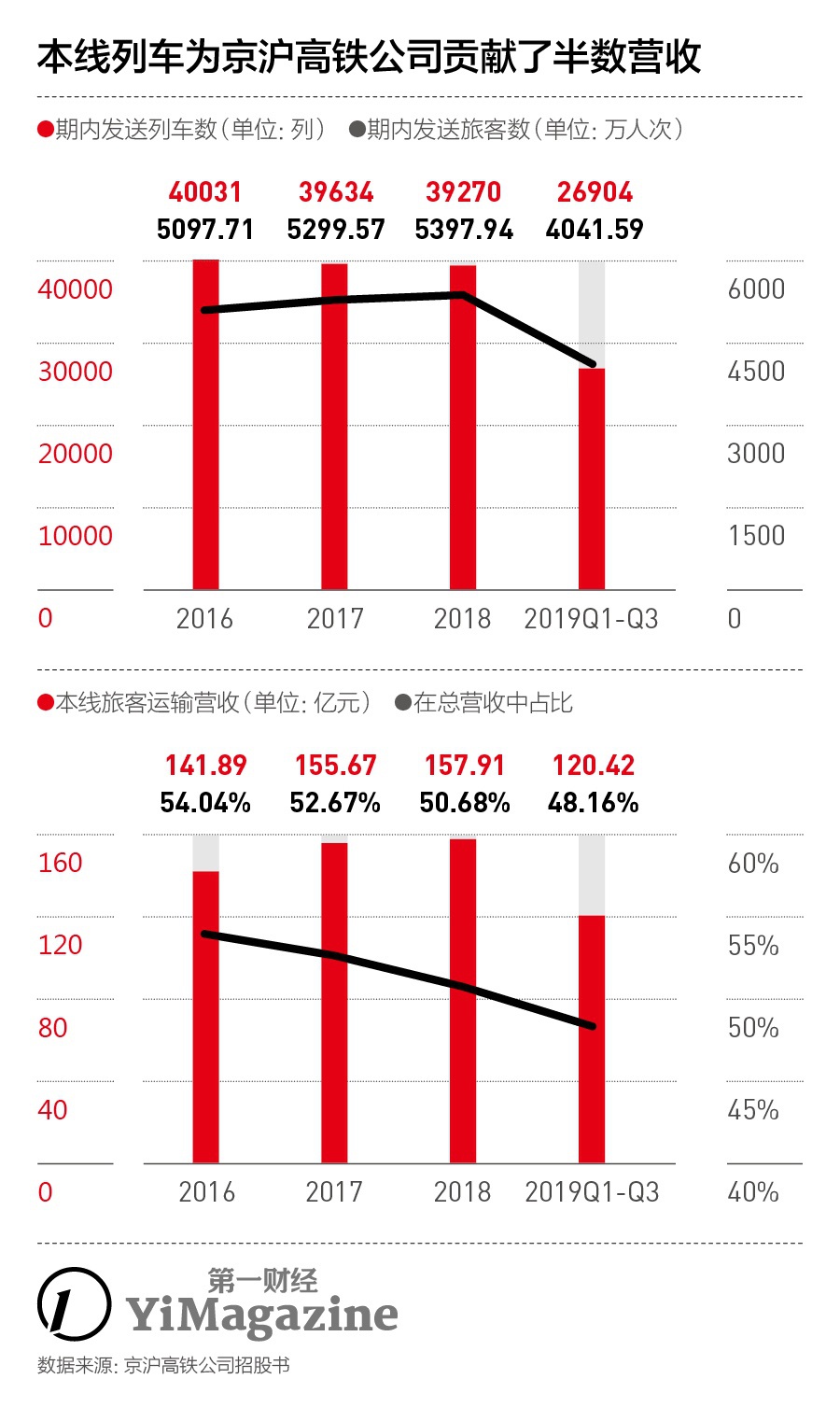

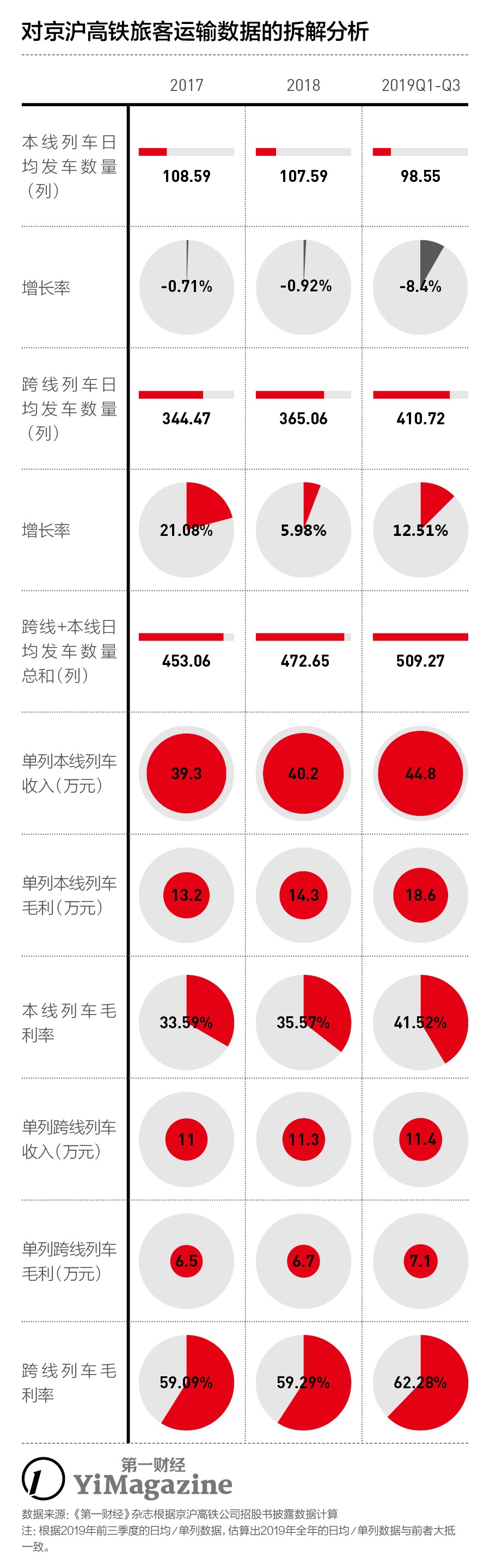

After the disclosure of the prospectus of Beijing-Shanghai high-speed rail, the outside world marveled at its annual income scale of more than 30 billion yuan. At present, the company’s "local business" and "cross-line business" revenue accounts for basically the same proportion. In the business model, these two parts of income correspond to completely different indicators and models.

The income of the "local train" is the fare, and the two indicators that affect the income are the total number of passengers sent and the average fare paid by passengers. However, the prospectus of Beijing-Shanghai high-speed railway does not directly disclose the average passenger fare, but only discloses the passenger transportation data such as the total number of trains sent, the number of passengers sent, the load factor and the passenger turnover during the reporting period.

The main factor that affects the income of "cross-line trains" is the number of trains that purchase services from the road network. According to the prospectus, since the Beijing-Shanghai high-speed railway line is connected with many high-speed railways such as Jingha, Taiqing and Shanghai-Kunming, and the hub stations along the line are mostly traffic hubs in the eastern region, with the gradual improvement of the high-speed railway network, the corresponding cross-line train income has also increased.

Since 2016, the actual controller of Beijing-Shanghai high-speed rail — — China Railway Corporation, the predecessor of China National Railway Group Co., Ltd. (hereinafter referred to as "China State Railway Group Co.,Ltd."), has the "pricing power" for high-speed rail, and can implement certain fare fluctuations according to factors such as market competition and passenger flow distribution. In the past few years, although there have been preferential discount tickets for high-speed rail and bullet trains as a whole, the fares of key lines represented by Beijing-Shanghai high-speed rail have remained unchanged for many years.

A more noteworthy variable is that in recent years, with the introduction of the "Fuxing" train with faster running speed, the opening of long-formed trains that can accommodate more passengers, and the adjustment of the proportion of trains with various formation sizes, the annual total number of passengers sent by trains on this line is steadily increasing, but the daily average number of trains on this line is declining.

This idea of small-scale adjustment is believed to continue in the next year or two and become an important variable affecting the company’s revenue and gross profit growth. On the premise that the ticket price is relatively constant, CBN magazine calculated the annual revenue and gross profit growth range of Beijing-Shanghai high-speed rail in the future. Under optimistic circumstances, it is estimated that the annual growth rate of its revenue will reach 9.34% and the gross profit will increase by 7.55%. Even in a relatively pessimistic situation, the performance can remain stable.

The core asset of Beijing-Shanghai high-speed railway company is the high-speed railway network. Considering the minimum train tracking interval, train speed and other factors, its overall capacity has a theoretical upper limit. In order to maximize the growth of revenue and profit, the company should actually consider how to balance the proportion of local cars and cross-line cars.

In the routine inquiry of the CSRC about the prospectus of Beijing-Shanghai high-speed rail, one question is to ask the company to explain whether the second line of Beijing-Shanghai high-speed rail may form a major horizontal competition relationship with the existing business. As the bidding for related design projects was publicized, the second line of Beijing-Shanghai high-speed rail, which is still in early planning, happened to catch up with the "hot spot" of listing of Beijing-Shanghai high-speed rail. In order to alleviate the transportation pressure of Beijing-Shanghai high-speed rail, the National Development and Reform Commission announced the development plan of the future high-speed rail in July 2016, and the "Beijing-Shanghai Passage" part involved is the Beijing-Shanghai Second Line. Except the origin and destination stations and Tianjin section are consistent with the current Beijing-Shanghai line, Weifang, Linyi, Huai ‘an, Yangzhou and Nantong on the Beijing-Shanghai second line are all closer to the east coast of China. These two railway lines connecting Beijing and Shanghai will become an important part of the "eight verticals and eight horizontals" long-term planning of China railway network in the future. As more high-speed rail lines are built and merged into the existing network, the utilization rate of the existing Beijing-Shanghai high-speed rail line will further increase, but the cost will decrease according to the marginal effect, thus gradually pushing up the gross profit margin.

Close to "big profit"

In the railway industry, there are so-called "small profits" and "big profits". "Small profit" means that income can offset operating costs, such as labor, energy, depreciation, etc. The "big profit" is based on the investment in railway construction, such as loan interest and principal.

Due to the huge construction cost, in addition to the capital invested by the company’s shareholders, high-speed rail projects often rely on a large number of debt financing to fill the gap. When the Beijing-Shanghai high-speed railway was built, 50% capital and 50% loans and bonds were used to cover the upfront cost of 220 billion yuan. According to the prospectus, as of the end of the third quarter of 2019, the Beijing-Shanghai high-speed railway still has a total of 21.807 billion yuan of long-term loans, of which 1.5 billion yuan will expire within one year; It is estimated that in the whole year of 2019, the company will still have to pay more than 1 billion yuan in interest on the loan.

For the Beijing-Shanghai High-speed Railway Company, there is a relatively objective profit margin for ticket and road network revenue. According to the prospectus, the current interest guarantee multiple (editor’s note: earnings before interest and tax’s interest expenditure, which is used to measure the company’s basic ability to repay loans) is 16 times. In addition, the company repaid 7.5 billion yuan of long-term loans in advance in 2016, so it is quite promising to achieve the "big profit" goal of "paying interest and repaying principal".

But this is only the result of independent inspection of high-speed rail operating companies. Because of the close cooperation between the high-speed rail operating company and the railway bureau, it is difficult to analyze it independently in daily operation, so the influence of the railway bureau should be considered when investigating the overall operation of the high-speed rail line.

The prospectus of the Beijing-Shanghai High-speed Railway also disclosed some operation data of 18 railway bureaus under the jurisdiction of China State Railway Group Co.,Ltd.. Among the three railway bureaus in Beijing, Jinan and Shanghai involved in the line, in 2018, only the Shanghai Bureau had a profit of 1.7 billion yuan, the Jinan Bureau suffered a slight loss, and the Beijing Bureau had a loss of 6.139 billion yuan. The income and profit level of the specific line were not disclosed. And China State Railway Group Co.,Ltd.’s total debt level has stabilized at more than 5 trillion yuan.

According to the report "China’s High-speed Railway Development" released by the World Bank in mid-2019, if the overall profitability of the lines composed of "corresponding investment from operating companies and railway bureaus" is investigated, many lines with a design speed of 200-250km/h in China can hardly achieve the operation goal of "small profit" at the initial stage of opening. After the line is opened for 10 years, the principal and interest pressure has been significantly reduced, and more than half of the lines with a design speed of 300 to 350 kilometers per hour can achieve "big profits" at the existing passenger traffic level.

Of course, there is also the debt borne by local governments for the introduction of high-speed rail. In order to implement the relevant demolition funds, local governments rely heavily on bank loans in addition to using financial funds, which actually further increases their own burden. In 2018, the Development and Reform Commission issued special guidance to warn individual places of the hidden debt risk under the "high-speed rail effect".

In the face of such an overall situation of the industry, as a star company entity with annual profits and dividends, IPO financing of 50 billion yuan and "promoting the reform of railway joint-stock system", the economic value of Beijing-Shanghai high-speed railway is remarkable, but it is impossible to copy it.

: No.1 is "Zhengzhou Publishing"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> Dong Yuhui knows Henan (released by Zhengzhou)</p>

<p> This illegal construction in our city was forcibly demolished (released by Sanmenxia)</p>

<p> Investigation from Gao Jianjun to Longevity Mountain Scenic Area (released in Kaifeng)</p>

<p> Notice of the Office of Pingdingshan Municipal People’s Government on the Holiday Arrangements for Labor Day in 2024 (released by Pingdingshan)</p>

<p> [May 1 Raiders] From now on, Xinxiang is full of heat! (Meet Xinxiang)</p>

<p> The ranking of WeChat WeChat official account in this list is: Zhengzhou Publishing, Sanmenxia Publishing, Xinyang Government Affairs, Nanyang Publishing, Kaifeng Publishing, Henan Zhengzhou Airport Publishing, Pingdingshan Publishing, Puyang Publishing, Zhumadian Publishing, Anyang Municipal Government Network, Jiaozuo Publishing, Shangqiu Publishing, Xuchang Publishing, Zhoukou Publishing, Meet Xinxiang, Hebi Government Affairs, Luohe Government Affairs, Luoyang Municipal Government Network and Jiyuan Government Affairs.</p>

<p style=)

: the number of the top scholar is "Jinshui Publishing"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> From now on, Science Avenue in High-tech Zone will be closed for construction! Please detour (Zhengzhou High-tech Release)</p>

<p> Voting | The online voting of the seventh moral model in Yuanyang County began (Yuanyang Rongmei)</p>

<p> Traffic control (released by Xinzheng)</p>

<p> Bulletin on the incident of "boy being dragged on horseback" in Xingyang City (released by Xingyang)</p>

<p> At this moment, the Yellow River North Street is beautiful! (Jinshui released)</p>

<p> The ranking of WeChat WeChat official account in this list is as follows: Jinshui Publishing, Erqi Publishing, Today Changge Publishing, Xinzheng Publishing, Huiji Publishing, Zhongmu Publishing, Yichuan News, Zhengzhou Zhongyuan Publishing, Xinmi Publishing, Today Ruyang Publishing, Gongyi Publishing, Luanchuan Media Integration, Shuo Biyang Publishing, Xingyang Publishing, Yanshi Media Integration, Dengfeng Publishing, Ruzhou City Affairs, Tangyin Media Integration, Zhengzhou High-tech Publishing, Wonderful Yu Publishing. Xin ‘an County Release, wugang city Rong Media Center, V Guan Mianchi, Guancheng Release, Yuanyang Rong Media, wen county Today, Songxian Rong Media, Yanjin Rong Media, Qingfeng Release, Shangjie Release, Dengzhou Headline, Qingqing Lushi, Lankao Mobile Phone Station, Qixian Release, China Jincheng Lingbao Rong Media, Qinyang Today, Xinxian Radio and Television Station, Longxiang Today, Minquan.com, Lankao Mobile Phone Station.</p>

<p style=)

: No.1 is "Anyang Education Bureau"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> A letter from Pingdingshan Education and Sports Bureau to all students and parents during the Tomb-Sweeping Day holiday in 2024 (Pingdingshan Education and Sports Bureau)</p>

<p> In 2024, the schools directly under Anyang Education Bureau openly recruited 60 teachers (Anyang Education Bureau).</p>

<p> Zhengzhou Education Bureau issued a warm reminder of the May 1 holiday → (Zhengzhou Education)</p>

<p> A letter from Xinxiang Education Bureau to the parents of the whole city during the May 1 holiday (Xinxiang Education Bureau)</p>

<p> May Day holiday off-campus training reminder! (Luoyang Education Bureau)</p>

<p> The ranking of WeChat WeChat official account in this list is: Anyang Education Bureau, Zhengzhou Education, Kaifeng Education and Sports, Pingdingshan Education and Sports Bureau, Puyang Education, Luohe Education Bureau, Xinxiang Education Bureau, Sanmenxia Education Bureau, Luoyang Education Bureau, Zhoukou Education and Sports Bureau, Xinyang Education Television, Nanyang Education Bureau, Jiaozuo Education Bureau, Jiyuan Education and Sports Bureau, Hebi Education and Sports Bureau, Shangqiu Education and Sports Bureau and Xuchang Education.</p>

<p style=)

: the number one is "Luoyang Tourism"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> At this moment, Dong Yuhui’s first stop is Luoyang! (Luoyang Tourism)</p>

<p> Guo Yuxuan from Anyang No.2 Middle School, 12 scenic spots are waiting for you! (Anyang Municipal Bureau of Culture, Radio, Film and Sports Tourism)</p>

<p> Do you want to visit Xinxiang Pangdong during the May Day holiday? In the face of "pouring traffic", Xinxiang "accepted"! (Xinxiang Wenlv)</p>

<p> Zhumadian scenic spot is free of tickets again! (Zhumadian Wenlv)</p>

<p> What? ? These A-level scenic spots in Zhengzhou are free! ! (Zhengzhou Wenlv)</p>

<p> The ranking of WeChat WeChat official account in this list is: Luoyang Tourism, Anyang Cultural Radio, Film and Television Sports Tourism Bureau, Kaifeng Cultural Radio and Television Tourism Bureau, Zhumadian Cultural Tourism Bureau, Xinyang Cultural Tourism Bureau, Jiaozuo Cultural Tourism Bureau, Xuchang Cultural Tourism Bureau, Zhengzhou Cultural Tourism Bureau, Xinxiang Cultural Tourism Bureau, Sanmenxia Cultural Tourism Bureau, Hebi Cultural Radio, Film and Television Tourism Bureau, Nanyang Cultural Tourism Bureau, Jiyuan Cultural Tourism Bureau, Pingdingshan Cultural Radio, Film and Television Tourism Bureau, Shangqiu Cultural Radio, Film and Television Tourism Bureau and Luohe Cultural Tourism Bureau.</p>

<p style=)

: the number one is "Luoyang Health and Health Commission"</b></p>

<p> Urgent notice! It is related to the re-examination of grassroots non-educated personnel in the national doctor qualification examination (healthy Zhengzhou)</p>

<p> A letter from Zhoukou test center of 2024 nurse qualification and health professional and technical qualification examination to candidates (Zhoukou Health and Health Committee)</p>

<p> Excellent immunization planners who "stick to 30 years" praise the channel is about to open! Come and like Ta! (Healthy Jiaozuo)</p>

<p> The ceremony for the 25th batch of medical teams from Nanyang to assist Zambian China was held ceremoniously (Nanyang Health and Sports Committee).</p>

<p> Healthy Kaifeng 100% Phase 30 (Healthy Kaifeng)</p>

<p> The ranking of WeChat WeChat official account in this list is: Luoyang Health and Health Committee, Healthy Zhengzhou, Luohe Health and Health Committee, Healthy Kaifeng, Healthy Shangqiu, Nanyang Health and Health Sports Committee, Healthy Jiaozuo, Zhoukou Health and Health Committee, Xinyang Health and Health Committee, Puyang Health and Health, Healthy Zhumadian, Healthy Jiyuan, Healthy Sanmenxia, Healthy Anyang, Healthy Xuchang, Hebi Health and Health, Xinxiang Health and Health Committee, Pingdingshan Health and Health Committee.</p>

<p style=)

: the number one is "Henan Medical Security Service Center"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> Notice on adjusting the business handling mode of the network hall of the provincial medical insurance public service platform unit (Henan Medical Security Service Center)</p>

<p> From now on, our county’s "outpatient chronic diseases" can be declared online at any time! (Ye County Medical Insurance Bureau)</p>

<p> Typical Cases Exposed by the Exposure Desk of Shangqiu Medical Security Bureau in Phase II (Shangqiu Medical Insurance Bureau)</p>

<p> [Medical Insurance Policy] The latest medical insurance policy for urban workers in Anyang (Anyang Medical Insurance)</p>

<p> Turn and expand! Check the overall balance of Luoyang staff outpatient service like this! (Luoyang Medical Insurance)</p>

<p> The ranking of WeChat WeChat official account in this list is: Henan Medical Insurance Service Center, Luoyang Medical Insurance, Anyang Medical Insurance, Shangqiu Medical Insurance Bureau, Kaifeng Medical Insurance, Xinxiang Medical Insurance, Puyang Medical Insurance Bureau, Yexian Medical Insurance Bureau, Zhengzhou Medical Insurance Bureau, Luohe Medical Insurance Bureau, Ruzhou Medical Insurance Bureau, Songxian Medical Insurance Bureau, Gushi County Urban and Rural Medical Insurance Center, Luanchuan County Medical Insurance Bureau, Zhoukou Medical Insurance Bureau, Xuchang Medical Insurance Bureau, Linzhou Medical Insurance Bureau, hua county.</p>

<p style=)

: No.1 is "Jiyuan Market Supervision"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> Jiyuan made a typical speech at the "two responsibility" training course on food safety in the whole province (Jiyuan market supervision)</p>

<p> City leaders investigate and guide the pre-holiday market supervision (Xinxiang market supervision)</p>

<p> Reminder of Anyang Municipal Market Supervision Administration on Regulating Market Price Behavior during the 2024 Anyang Marathon (Anyang Market Supervision)</p>

<p> Zhengzhou Municipal Market Supervision Bureau went to Xingyang to study and visit the Yellow River Crossing Project of the Middle Route of South-to-North Water Transfer Project (Zhengzhou Market Supervision)</p>

<p> A typical case of special action on campus food safety investigation and rectification in Luoyang (Luoyang market supervision)</p>

<p> The ranking of WeChat WeChat official account in this list is: Jiyuan Market Supervision, Hebi Market Supervision, Zhengzhou Market Supervision, Anyang Market Supervision, Kaifeng Market Supervision, Sanmenxia Market Supervision, Pingdingshan Market Supervision, Shangqiu Market Supervision, Xuchang Market Supervision, Nanyang Market Supervision, Luoyang Market Supervision, Luohe Market Supervision, Xinxiang Market Supervision, Zhumadian Market Supervision, Puyang Market Supervision, Xinyang Market Supervision, Jiaozuo Market Supervision Administration and Zhoukou Market Supervision.</p>

<p style=)

: the number one is "Common Office"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> Notice on Measures for Paying Government Subsidies for Deed Tax on Commercial Housing (Co-Office)</p>

<p> This is love Nanyang! (Nanyang government service)</p>

<p> In the first quarter of 2024, the questionnaire survey on people’s satisfaction with drug control work has been launched (Qixian Government Service and Big Data Administration)</p>

<p> Handling of mass appeals from March 21 to March 27, 2024 (Luoyang 12345 government service convenience hotline)</p>

<p> Weishi County Bureau of Politics and Statistics: Kaifeng Weishi and Airport Economic Comprehensive Experimental Zone held the signing ceremony of "cross-domain communication" of government services (Weishi government services).</p>

<p> The ranking of WeChat WeChat official account in this list is: Gongban, Nanyang Government Service, Yindu Government Service, Luoyang 12345 Government Service Convenience Hotline, Qixian Government Service and Big Data Administration, Hebi Government Service and Big Data Administration, Sanmenxia Government Service and Big Data Administration, lankao county Government Service and Big Data Administration, Hongqi District Government Service Center, mengzhou city Government Service and Big Data Administration, Weishi Government Service, Yuanhui Government Service, Zhumadian Municipal Government Service and Big Data Administration, Kaifeng Municipal Government Service, Shangshui County Government Service and Big Data Administration, Longan Government Statistics, Changyuan Government Service, Jiaozuo Administrative Approval and Government Information Administration, Xiangfu District Government Service and Big Data Administration, Tongxu Government Service.</p>

<p style=)

: The number one scholar is "Long live the Mountain Martial Arts City"</b></p>

<p> The articles with higher comprehensive ranking in this list and their WeChat WeChat official account are as follows:</p>

<p> Dong Yuhui walks into "Only Henan" and talks with Wang Chaoge: This is endless touching! (Only Henan Drama Fantasy City)</p>

<p> Announcement on "Wang Po Matchmaker" (Long Live the Martial Arts City)</p>

<p> Traveling on May Day, why choose a movie town? (Jianye Film Town)</p>

<p> You can visit Qingming Shanghe Garden for free on May Day! New performances, new scenes, more shocking and exciting, meet with you at the Puppet Carnival! (Kaifeng Qingming Shangheyuan Scenic Area)</p>

<p> Tips on booking a tour during the May Day holiday in Luoyang Baima Temple (Baima Temple in Luoyang)</p>

<p> The ranking of WeChat WeChat official account in this list is: Longevity Mountain Martial Arts City, Kaifeng Qingming Shangheyuan Scenic Area, Only Henan Drama Fantasy City, Virescence Expo, Jianye Film Town, Longmen Grottoes, Yuntai Mountain Scenic Area, Luoyang Baima Temple, Baoquan Scenic Area, Laojun Mountain Scenic Area, Encountering Sui and Tang Dynasties, Zhengzhou Fangte, Luoyang Sui and Tang Dynasties Ruins Botanical Garden, Yinji International Tourism Resort, Yinxu Scenic Area, Luoyang Baiyun Mountain and Luanchuan Zhuhai Wildlife Park. Taihang Grand Canyon, Luoyang Longtan Grand Canyon Scenic Area, Xinxiang Wan Xianshan Scenic Area, Henan Laojie Mountain, chaya mountain Scenic Area, Xinxiang South Taihang Baligou Scenic Area, Wenxin Tea Village, Henan Qixian Yunmeng Mountain Scenic Area, Hanguguan Tourist Area, Hanyuan Stele Forest, Wangwu Mountain, Danjiang Daguanyuan Scenic Area, Jigongshan Scenic Area, Shangqiu Riyue Lake Scenic Area, Wanquan Lake Scenic Area, Hongqi Canal Tourism, Shangqiu Ancient City Scenic Area and Jiguandong Scenic Area. Western Henan Grand Canyon Tourist Resort, Fengxiang Hot Spring, Huangdi’s Hometown, Shendong Ancient Town Scenic Area Guanwei, Fenghu Scenic Area, Erlang Mountain Scenic Area, Jingang Taixi River Tourism, Yellow River Rich Scenic Ecological World, Zhongyuan Futa and Gubaidu Tourist Resort.</p>

<p style=)

was produced by Dahewang Dahe Public Opinion Research Institute, and the monitoring objects covered WeChat official account, an active government wechat in Henan Province, and WeChat official account, a scenic wechat. The monitoring period was from April 1 to April 30, 2024. Please call 0371-61530121 if you are interested in promoting the construction of smart government affairs, or if you are interested in recommending yourself to include your government affairs WeChat WeChat official account in the monitoring scope. (Yang Huijun, Xu Jingyao, Zhan Ting, Wang Ying)</p>

<p></p>

<div class=)